If you’ve written a check to a vendor and reduced your account balance in your internal systems accordingly, your bank might show a higher balance until the check hits your account. Similarly, if you were expecting an electronic payment in one month, but it didn’t actually clear until a day before or after the end of the month, this could cause a discrepancy. The documentation review process compares the amount of each transaction with the amount shown as incoming or outgoing in the corresponding account. For example, suppose a responsible individual retains all of their credit card receipts but notices several new charges on the credit card bill that they do not recognize. Perhaps the charges are small, and the person overlooks them thinking that they are lunch expenses. As noted earlier, your state may have specific requirements for how often you must conduct three-way reconciliation—such as monthly or quarterly.

- Financial professionals must be vigilant in identifying and correcting discrepancies due to bank errors, accounting mistakes, and instances of fraud and theft.

- Effective reconciliation of bookkeeping accounts is essential for maintaining accurate financial records.

- If there are receipts recorded in the internal register and missing in the bank statement, add the transactions to the bank statement.

- Let’s take a look at a hypothetical company’s bank and financial statements to see how to conduct a bank reconciliation.

Business reconciliation

The individual is reimbursed for the incorrect charges, the card is canceled, and the fraudulent activity stopped. All trust transactions in the internal ledger should be accurately recorded and should align with transactions in the individual client ledgers. Once you have access to all the necessary records, you need to reconcile, or compare, the above the line below the line financial concept internal trust account’s ledger to individual client ledgers. Find direct deposits and account credits that appear in the cash book but not in the bank statement, and add them to the bank statement balance.

Identify Discrepancies

Bank reconciliation statements are also important for alerting a company in case of fraud or error. To be effective, a bank reconciliation hire quickbooks consultant statement should include all transactions that impact a company’s financial accounts. A bank reconciliation is an essential process for ensuring that your company’s financial statements match the available cash in your business bank account. Performing regular bank reconciliations helps you stay on top of cash flow, keep organized records for tax season, and minimize the risk of fraud and theft. We’ll explore the definition of bank reconciliation, why it’s important, and a step-by-step process for performing bank reconciliations. We’ll also look at common sources of discrepancies between financial statements and bank statements to help you identify fraud risks and errors.

A bank reconciliation is used to detect any errors, catch discrepancies between the two, and provide an accurate picture of the company’s cash position that accounts for funds in transit. In general, reconciling bank statements can help you identify any unusual transactions that might be caused by fraud or accounting errors. Legal software for trust accounting can help you track transactions and reconcile records and bank statements. Clio’s legal trust management software, for example, allows you to manage your firm’s trust accounting, reconcile directly in Clio, and run built-in legal trust account reports. Bank reconciliation is an accounting process where you compare your bank statement with your own internal records to ensure that all transactions are accounted for, accurate, and in agreement. By catching these differences through reconciliation in accounting, you can resolve discrepancies, help prevent fraud, better ensure the accuracy of financial records, and avoid regulatory compliance issues.

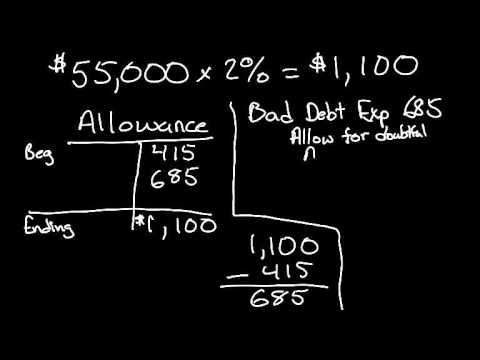

For the current year, the company estimates that annual revenue will be $100 million, based on its historical account activity. The company’s current revenue is $9 million, which is way too low compared to the company’s projection. While scrutinizing the records, the company finds that the rental expenses for its premises were double-charged.

What is the typical format used for reconciliation accounts?

While proper reconciliation is the standard for how law firms should handle all financial accounts, it is particularly important—and often required—for the management of trust accounts. Reconciliation must be performed on a regular and continuous basis on all balance sheet accounts as a way of ensuring the integrity of financial records. Reconciling the accounts is a particularly important activity for businesses and individuals because it is an opportunity to check for fraudulent activity and to prevent financial statement errors. Reconciliation is typically done at regular intervals, such as monthly or quarterly, as part of normal accounting procedures.

Performing regular what is inventory valuation and why is it important bank reconciliations is key to keeping on top of your company’s financial health and paving the way for sustainable business growth. On a regular basis, usually at the end of each month, bookkeepers or accountants review each account in the general ledger. The review involves matching the ledger’s transactions against external records, such as bank statements.

Unpredictable interest income may also be a challenge when calculating financial statements, which can lead to challenges during a bank reconciliation. Bank charges are service charges and fees deducted for the bank’s processing of the business’s checking account activity. If you’ve earned any interest on your bank account balance, it must be added to the cash account.